December 28, 2023

On Wednesday, December 13, the Fed issued it’s latest statement. While Chairman Powell continued to stress fighting inflation, he indicated that interest rate cuts are possible in 2024. In fact, as many as three 0.25% cuts seem possible.

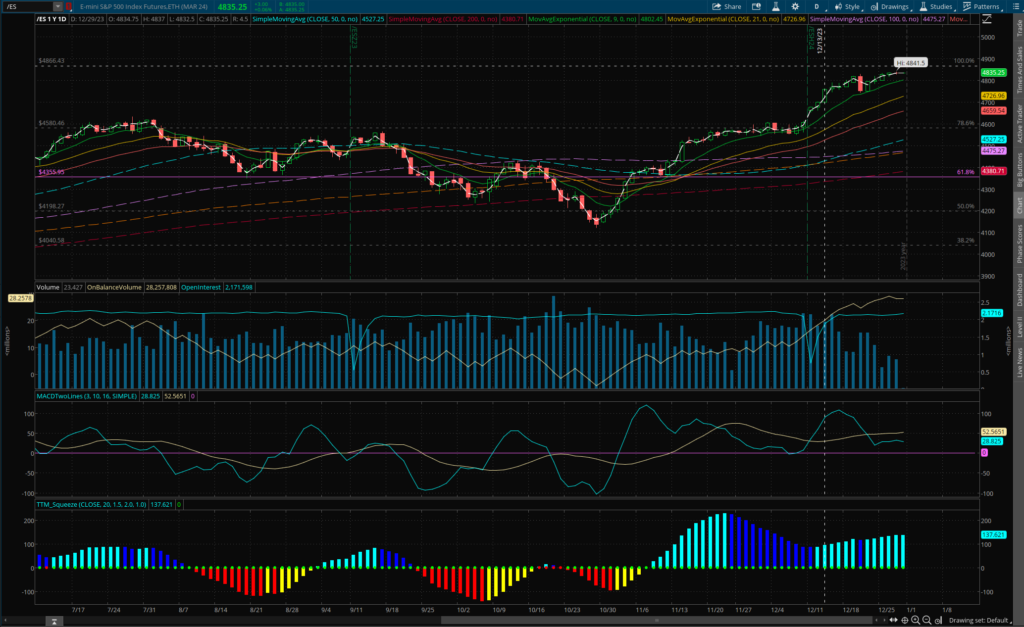

This was, in fact, a major sea change for markets and set off a major rally into the end of the year. As of this evening, the S&P futures stand at 4,841, up 3% from 4,700 the day before the Fed statement on December 13, 2023.

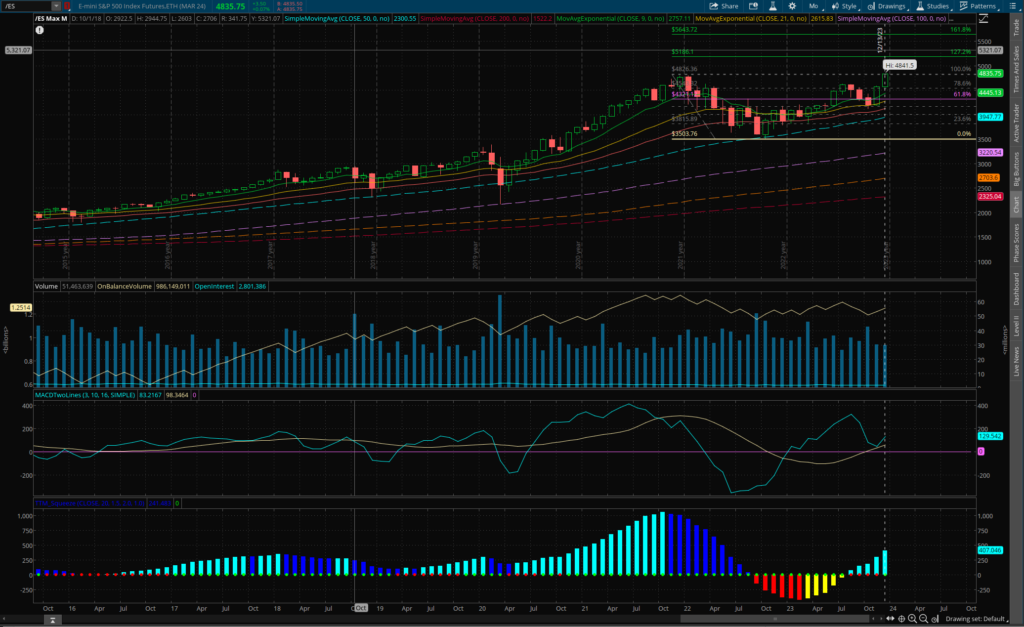

To better understand the significance of this rally, let’s take a look at a longer term monthly chart, below. You’ll see that we’ve exceeded the highs from December 2021 – January 2022, and in fact, we’re at new all-time highs.

Why such a rally? Before the Fed statement, the market believed that the economy was weakening and predicted three or more rate cuts were necessary in 2024. Many believed that with the fight against inflation not yet over, the Fed would push back against the market and say that rates needed to stay high, and that three rate cuts in 2024 was far too much. In this most recent statement, the Fed said the opposite and indicated that three rate cuts was actually a possibility. In short, the Fed seemed to come around to the market’s point of view. This led many to declare that the Fed was finished raising rates, and that the Fed had indeed, engineered a “soft landing” – that the Fed had successfully fought inflation without substantially weakening the economy.

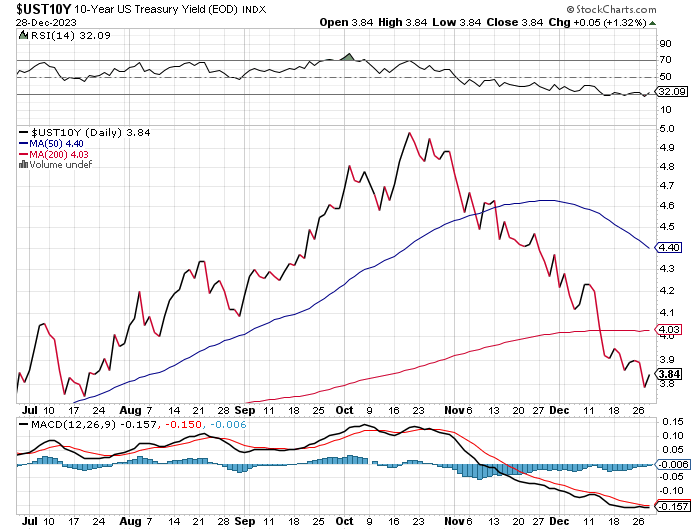

Nowhere was this sentiment more evident than in the bond market, where 10 year yields had fallen from nearly 5% in October to under 4% in December. In short, the bond market believes that the Fed no longer needs to increase interest rates to fight inflation, and in fact, money is now coming out of the bond market and into the stock market.

Implications for 2024

So what does this mean for 2024? I think it’s hard to predict, but let’s take a look at the bullish and bearish factors that we know of. On the bullish side:

First, in the absence of clearly bad news, bullish trends tend to continue. This is in part because many people are caught off-sides, so the rising market tends to pull cash into the market.

Second, while many are surprised that corporate earnings are generally good, I’m not at all surprised. Why? Because prices have jumped, and while there are some indications that the consumer is weakening, the consumer is still making do. That means all those profits from higher prices are going to the corporations. As long as the consumer does not fall apart, corporations will keep prices high and continue to benefit.

So how far can this rally go? Of course, no way to know for sure, but using Fibonacci extensions – the ratios commonly used by professionals – the market now targets 4,948 in the near term (technically, this is known as the 1.68 extension of the current swing). This is about 100 points above today’s current value.

What about the bearish forces? Well for the moment, we only have a technical driver – the market is overbought after a sharp run-up. Things can’t be sharply upward sloping forever, so the recent trend is likely to taper in the coming weeks.

As the calendar turns, there is likely to be some profit taking. Those that did not want to sell in December and recognize a tax profit can do so in January 2024.

Also, earnings are coming up. If you have a significant profit in any holdings, it makes sense to take some off the table in case earnings – which are based on future expectations – are not favorable.

Conclusions

On the whole, the market is relatively bullish. The Fed seems to be on hold, which is what the market wants, and both corporations and consumers seem to be doing well and well enough. While there could be some selling pressure in January / February, the weight of the market drivers is with the bulls.

Disclaimer. The content {“Content”) on this website (the “Site”) is for informational purposes only. You should not construe any such information or other material as legal, tax, investment financial or other advice. Readers are urged to consult their own financial counselors before making any investment decisions. The author is not a fiduciary by virtue of any person’s use or access of the Site or its Content. You alone assume sole responsibility for evaluating the merits or risks associated with the use of any information on this Site. In exchange for using the site, you agree not to hold the author, his affiliates, or any other third party service provider liable for any possible claim for damages arising from any decision you make based on the information or Content found on the Site. All material presented herein is believed to be accurate but the author cannot attest to its accuracy. There is no certainty that any of the information, charts or graphs presented here would result in profits. Opinions expressed may change without prior notice. The author may or may not have investments in the stocks or sectors mentioned.

Leave a Reply